While the global scientific community’s consensus may be enough justification for some, in 2021 the Biden administration made clear its view that climate change is a significant national security challenge. One can look to the Annual Threat Assessment of the U.S. Intelligence Community, the Department of Defense’s Climate Risk Analysis, and the Department of Homeland Security’s Strategic Framework for Addressing Climate Change that underscore the seriousness of the concern. These statements set high level intentions and outline strategic measures for the United States but are agnostic about the role that technology can play in addressing the threat of climate change. Climate change sits squarely at the intersection of technology and national security, with both the causes and the potential solutions to climate change being largely a function of humanity’s technology choices.

Climate change has both direct and indirect consequences for U.S. national security. Drought and crop failure linked to climate change influences global conflict and migration already. Many scientists believe climate change is making hurricanes, tornadoes, floods, and wildfires in the U.S. more frequent and more severe. Indirect consequences include macroeconomic and geopolitical impacts of shifting the global economy away from fossil fuels and emerging nation state competition to control the critical technologies and resources of the future global economy. The attention paid to climate change is also spinning off innovations with direct uses in the defense and national security realm. This is a good thing.

Climate technology, per the UN Environment Programme, is “any piece of equipment, technique, practical knowledge or skills for performing a particular activity that can be used to face climate change.” While this is a broad definition, we group climate technologies into four areas for our purposes:

- Observation and tracking using remote sensing such as satellite imaging, local sensors, and digital analytics to identify and evaluate changes to the natural world and human activity.

- Clean alternatives to decarbonize energy, transportation, housing, manufacturing, agriculture and other segments of the economy.

- Resource technologies that enable the location, mining, processing, recycling, and re-use of the lithium, cobalt, copper, rare earth metals, and other materials that the future economy will require.

- Adaptation and mitigation technologies such as carbon capture and storage to reduce the impacts of greenhouse gas emissions or technologies to help people live with the climate change impacts that are already unavoidable.

Boom and Bust

The Venture Capital community has finally shaken off the hangover from the “Cleantech” boom and bust of 2006-2012. Between 2005 and 2008, clean energy startup financing leapt from $300-500 million dollars a year to around $4 billion, before falling precipitously after 2012 to around $1-$1.5 billion. Several factors converged to create this burst of enthusiasm for cleantech investments, including growing public awareness of climate change, high oil and gas prices, idealistic investors looking to “give back” to society, and supportive Federal and state-level laws and policies such as tax credits, renewable energy mandates, and loan guarantees. The expectation was that the newly elected Obama administration would do even more to advance adoption. That bubble burst with the inevitable (in hindsight) decline in oil and gas prices, the failure to pass a cap-and-trade bill, controversy over loan guarantee losses, and—perhaps most importantly—worldwide over-investment in factories for solar panels, batteries and other technology that crashed prices and drove many clean energy startups out of business.

Not surprisingly, VC investors lost money on a lot of their Cleantech investments, which yielded lower returns even when they were successful and were more likely to fail than investments in software or healthcare companies. These investments failed for many reasons: some of the technology failed to scale, but difficult market conditions and weaker than expected government support also stunted companies’ growth and discouraged investors.

Even though VC investors often lost money, the “cleantech” markets turned out to be wildly successful. For example, the solar power market has grown 10x since 2010, reaching $130 billion per year even as prices fell by 85%, and the wind power market has quadrupled to over $60 billion while costs were cut in half. Global electric vehicle sales more than doubled from 2020 to 2021 and may exceed 10% of new car sales worldwide in 2022.

Venture Capital Returns to Climate Change

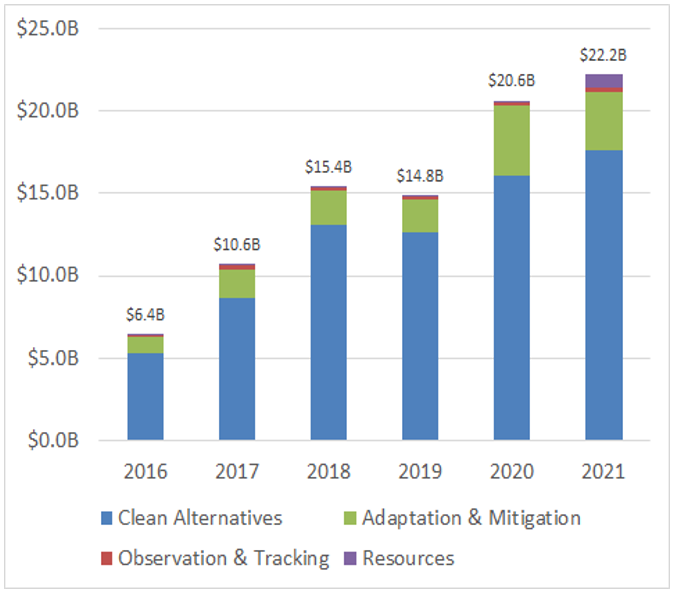

As public awareness and concern over climate change has increased and some “cleantech 1.0” companies like Tesla and Beyond Meat have delivered strong returns for their investors, venture capital has returned to the climate technology space. VC investment in climate tech has grown steadily since 2016 and now exceeds $20 billion annually, but things are a little different this time:

- The focus is broader. Most of the money is still flowing to what we call “clean alternatives,” but a growing share is going into adaptation and mitigation, resources and observation and tracking as well. Even within clean alternatives VC investors are taking a broader look and backing companies focused on food and agriculture, climate-friendly industrial processes, and electrified transportation.

- Technologies and markets have matured. It’s a lot clearer now where the market opportunities lie, companies are less dependent on government support, and consumers have become more willing to pay a premium to reduce their climate footprint.

- Investors have learned some lessons and are backing more experienced management teams with more robust business plans and a more realistic understanding of the risks.

This trend shows no signs of slowing down. IQT has identified over $36 billion of VC funds with “vintage” 2016 or later investments that count climate as part of their core investment thesis. Over $12 billion of this was raised in 2021 alone so there is plenty of “dry powder” available. Generalist VC funds have raised at least $45B that has been invested in “climate tech” companies with hundreds of billions managed by pension funds, endowments, sovereign wealth funds, and other deep-pocketed institutions that are investing in later-stage climate tech companies.

International Competitiveness

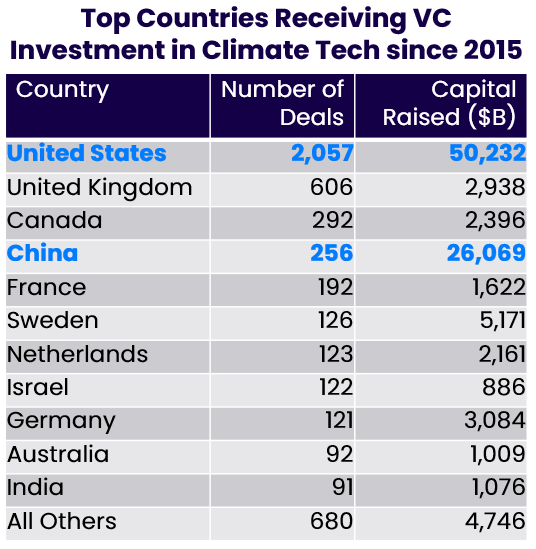

The U.S. is home to more innovative, well-capitalized climate tech companies than any other country and has established a strong position as a climate tech innovation leader, but that position is not assured. American companies have attracted about half of the VC investment dollars going into climate tech in the past six years; in fact, the U.S. is headquarters to – by far – the most climate tech “unicorns.” China is the clear #2 on both of these metrics and much of the supply chain for the raw materials and the manufacturing capacity for products like solar panels, batteries, and electric vehicles is now located in China. China’s climate tech industries rely heavily on Western technology, but China’s scientists, entrepreneurs, and investors are increasingly focused on developing their own technology. China has set growing the climate technology sector as one of its top priorities for the next decade.

Conclusion

The future of humanity depends on finding ways to deal with climate change, and investors are rising to the occasion. After a rough start 10 or 15 years ago, climate technology now seems poised for success. The markets are huge, the public wants solutions, and governments are supportive. Entrepreneurs and investors are piling into the sector and innovating broadly.

It’s important to remember though that there is more at stake here than money. Climate technologies—which will touch everything from housing and transportation to the food supply and military operations—are one of the commanding heights of the future economy, and they are going to become an important driver of geopolitics, economic and national security, just as fossil fuels have been for the past 100 years.